Executive Summary

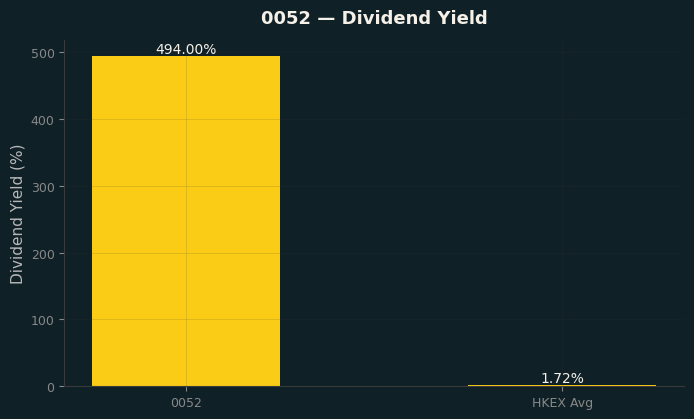

Fairwood Holdings Limited (0052.HK) reported a solid turnaround year for FY2025/2026 (year ended 31 March 2026), delivering a 17% increase in net profit to HK$41.6 million despite flat revenue of HK$3,098.8 million. The improvement was driven by a meaningful expansion in gross margin — from 7.7% to 8.7% — as the Group’s multi-year cost optimisation programme reached fruition across rent, labour, and operating expenses. A significantly higher final dividend of HK25.0 cents (FY2025: HK17.0 cents) brings the full-year DPS to HK30.0 cents, implying a near-full payout ratio of ~94% and a dividend yield of approximately 7.1% at the current share price (~HK$4.24).

| Key Metric | FY2026 | FY2025 | YoY |

|---|---|---|---|

| Revenue | HK$3,098.8M | HK$3,100.1M | -0.04% |

| Gross Profit | HK$268.4M | HK$237.2M | +13.2% |

| Gross Margin | 8.7% | 7.7% | +1.0pp |

| Operating Profit | HK$84.3M | HK$72.3M | +16.5% |

| Net Profit | HK$41.6M | HK$35.5M | +17.0% |

| Basic EPS | HK32.08¢ | HK27.43¢ | +17.0% |

| DPS (Full Year) | HK30.0¢ | HK22.0¢ | +36.4% |

| Payout Ratio | ~94% | ~80% | — |

| Cash & Bank Deposits | HK$575.3M | HK$545.7M | +5.4% |

Despite minimal top-line growth, the margin expansion story is credible and suggests the Group has structurally lowered its cost base. The key question remains whether Fairwood can translate this leaner operating model into profitable top-line growth — particularly in Mainland China, where losses persist but are narrowing.

1. Financial Performance Analysis

1.1 Revenue by Segment

Revenue was essentially flat year-on-year (-0.04%), with Hong Kong restaurants stable and Mainland China operations showing modest growth from an expanded store footprint.

| Segment | FY2026 Revenue (HK$M) | FY2025 Revenue (HK$M) | YoY |

|---|---|---|---|

| Hong Kong Restaurants | 2,929.2 | 2,932.7 | -0.1% |

| Mainland China Restaurants | 163.1 | 161.0 | +1.3% |

| Property Rental | 6.5 | 6.4 | +1.6% |

| Total | 3,098.8 | 3,100.1 | -0.04% |

Hong Kong same-store sales were likely slightly negative given the net addition of 3 Fairwood stores (to 150) with flat aggregate revenue. Mainland China revenue grew despite the segment still being in loss-making territory, reflecting the aggressive store expansion (+9 stores YoY to 28).

1.2 Cost Structure & Margin Analysis

The margin improvement — a rare bright spot in HK F&B — was achieved across all three major cost lines:

| Cost Line | FY2026 HK$M | % of Rev | FY2025 HK$M | % of Rev | Change |

|---|---|---|---|---|---|

| Food & Packaging | 763.7 | 24.6% | 750.1 | 24.2% | +0.4pp |

| Staff Costs | 1,092.7 | 35.3% | 1,096.2 | 35.4% | -0.1pp |

| Rental Costs* | 470.5 | 15.2% | 480.8 | 15.5% | -0.3pp |

| Total 3-Bucket | 2,326.9 | 75.1% | 2,327.1 | 75.1% | — |

| Other Opex & D&A | 503.5 | 16.2% | 535.8 | 17.3% | -1.1pp |

*Rental costs include depreciation on right-of-use assets, finance cost of lease liabilities, short-term leases, and variable lease payments.

Key observations:

- Staff costs were trimmed by ~HK$3.5M despite no reduction in headcount (~5,500), reflecting better manpower deployment via data-driven scheduling and multi-role tasking.

- Rental costs fell by HK$10.3M (~2.1%) following aggressive landlord negotiations and store network optimisation. The depreciation charge on right-of-use assets also declined from HK$419.5M to HK$410.6M.

- Food costs rose as a percentage of revenue (+0.4pp) as the Group invested in higher-quality ingredients for signature products — a deliberate strategic trade-off to drive brand perception and repeat visits.

- Other operating expenses (utilities, R&M, sanitation) all declined, demonstrating broad-based cost discipline.

1.3 Profit Bridge

| Item | FY2026 (HK$M) | FY2025 (HK$M) | Comment |

|---|---|---|---|

| Gross Profit | 268.4 | 237.2 | +31.2M from cost optimisation |

| Other Revenue / Net Gain | 33.6 | 58.2 | -24.6M, mainly lower lease modification gains |

| Selling Expenses | (41.2) | (43.7) | -2.5M |

| Administrative Expenses | (149.9) | (141.9) | +8.0M (new IT systems) |

| Impairment (PPE + ROU) | (27.5) | (36.4) | +8.9M improvement |

| Valuation on Inv. Properties | 0.8 | (1.2) | +2.0M swing |

| Operating Profit | 84.3 | 72.3 | +12.0M (+16.5%) |

| Finance Costs | (32.6) | (33.7) | -1.0M |

| Profit Before Tax | 51.6 | 38.6 | +13.0M (+33.6%) |

| Income Tax | (10.1) | (3.1) | +7.0M (deferred tax charge) |

| Net Profit | 41.6 | 35.5 | +6.1M (+17.0%) |

The tax charge jumped from HK$3.1M to HK$10.1M, primarily due to a deferred tax charge of HK$6.3M (reversal of prior-year deferred tax assets). On a pre-tax basis, profit grew 33.6% — significantly stronger than the 17.0% headline net profit growth would suggest.

2. Balance Sheet Analysis

| Line Item (HK$M) | 31 Mar 2026 | 31 Mar 2025 | Change |

|---|---|---|---|

| Investment Properties | 21.9 | 21.1 | +0.8 |

| Property, Plant & Equipment | 466.7 | 433.1 | +33.6 |

| Right-of-Use Assets | 890.7 | 881.0 | +9.7 |

| Goodwill | 1.0 | 1.0 | — |

| Total Non-Current Assets | 1,439.9 | 1,402.1 | +37.8 |

| Inventories | 56.9 | 54.3 | +2.6 |

| Trade & Other Receivables | 98.5 | 103.2 | -4.7 |

| Cash & Bank Deposits | 575.3 | 545.7 | +29.6 |

| Total Current Assets | 731.7 | 703.2 | +28.5 |

| Trade & Other Payables | 425.5 | 402.5 | +23.0 |

| Lease Liabilities (Current) | 365.2 | 372.4 | -7.2 |

| Bank Borrowings (Current) | 0.2 | 5.4 | -5.2 |

| Total Current Liabilities | 819.6 | 812.7 | +6.9 |

| Net Current Liabilities | (87.9) | (109.5) | +21.6 improvement |

| Lease Liabilities (Non-Current) | 580.2 | 565.7 | +14.5 |

| Bank Borrowings (Non-Current) | 5.3 | — | +5.3 |

| Provisions & LSP | 86.9 | 73.1 | +13.8 |

| Total Equity | 668.7 | 652.0 | +16.7 |

Key observations:

- Cash-rich, low-geared: Cash and bank deposits of HK$575.3M represent ~86% of total equity. Total bank borrowings are just HK$5.6M, giving a near-zero gearing ratio of 0.8%. Unutilised banking facilities stand at HK$351.1M.

- Net current liability position: The Group technically has net current liabilities of HK$87.9M, but this is entirely attributable to the classification of HK$365.2M in lease liabilities as current. Operating cash flow of HK$668.8M annually more than covers short-term obligations — the going concern is not in question.

- Lease-heavy balance sheet: Total lease liabilities of HK$945.4M dominate the liability structure, a function of the Group’s 184-store network. Right-of-use assets (HK$890.7M) broadly match these obligations.

- PPE increase: The HK$33.6M increase in PPE reflects HK$152.7M in capital expenditure (new stores, renovations, IT systems), partially offset by depreciation and impairments.

- Working capital: Trade receivables remain small at HK$8.4M (predominantly cash-and-carry F&B model). Trade payables of HK$119.6M are well-managed with 89% within 30 days.

3. Cash Flow & Capital Allocation

While the full cash flow statement is not reproduced in the announcement, key disclosures reveal strong cash generation:

| Item | FY2026 | FY2025 | Comment |

|---|---|---|---|

| Net Cash from Operations | HK$668.8M | HK$586.5M | +14.0%, well above reported profit |

| Capital Expenditure | HK$152.7M | HK$157.7M | -3.2%, disciplined spend |

| Dividends Paid | HK$28.5M | HK$45.3M | Interim + prior-year final |

| Cash Balance | HK$575.3M | HK$545.7M | +5.4% |

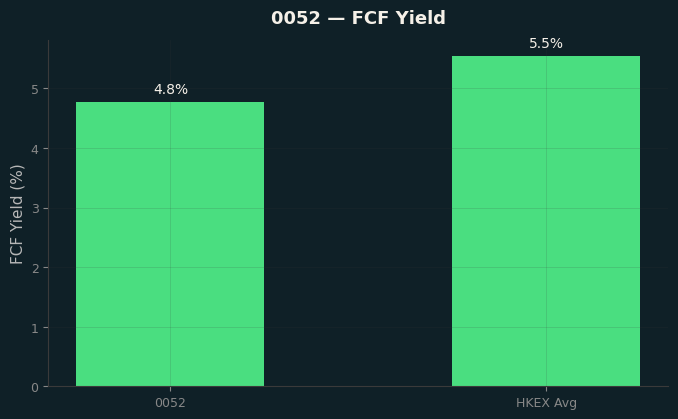

Operating cash flow of HK$668.8M dwarfs reported net profit of HK$41.6M due to significant non-cash depreciation charges (~HK$517.6M) flowing through the P&L. This is typical for an asset-heavy restaurant operator with substantial right-of-use asset amortisation.

Capital allocation priorities: The Group is balancing three uses of cash — (a) maintenance and growth capex (~HK$153M), (b) high dividend payouts (94% payout ratio, ~HK$38.9M proposed), and (c) balance sheet strengthening. With cash comfortably exceeding total borrowings by >100×, the generous dividend policy is well-supported.

4. Business Segment Review

4.1 Hong Kong Restaurants (94.5% of Revenue)

| Metric | FY2026 | FY2025 | Change |

|---|---|---|---|

| Revenue | HK$2,929.2M | HK$2,932.7M | -0.1% |

| Segment Profit | HK$81.6M | HK$64.5M | +26.5% |

| Segment Margin | 2.8% | 2.2% | +0.6pp |

| Fairwood Fast Food Stores | 150 | 147 | +3 |

| Specialty Restaurants | 6 | 6 | — |

The Hong Kong segment delivered a strong profit recovery through margin expansion. Key initiatives included:

- Signature product upgrades: Enhanced Ah Wood curry series, thicker-cut Baked Pork Chop Rice, improved breakfast egg dishes — driving quality perception and repeat visits.

- Store network optimisation: Strategic consolidation of underperforming locations, new store openings guided by data analytics (demographics, competitor mapping, market potential).

- Brand revitalisation: New “Jumping Man” logo rolled out; 4th and 4.5-generation store designs now represent >40% of the network, featuring modern aesthetics, self-service water stations, and BBQ stations.

- Digital & targeted marketing: KOL-driven social media campaigns, differentiated promotions by customer segment (value-seekers vs. convenience-seekers), Fairwood member app for engagement.

- Brand recognition: Multiple awards — IAB HK Digital Awards 2025, Marketing Excellence Awards 2025, Markies Awards 2026, Loyalty & Engagement Awards 2026.

The specialty restaurant portfolio (3 ASAP, 2 Leaf Kitchen, 1 Ombra) has completed brand consolidation, with ongoing work to enhance operational efficiency.

Soft Meals initiative: All 150 Fairwood stores now offer soft meals for the elderly and those with swallowing difficulties — 8 flavors available. Endorsed by HKU’s Swallowing Research Laboratory. Positioned as both a social responsibility initiative and a market differentiator.

4.2 Mainland China Restaurants (5.3% of Revenue)

| Metric | FY2026 | FY2025 | Change |

|---|---|---|---|

| Revenue | HK$163.1M | HK$161.0M | +1.3% |

| Segment Loss | HK$(16.6)M | HK$(22.5)M | -26.2% improvement |

| Stores | 28 | 19 | +9 (+47%) |

The Mainland China segment remains in investment mode but is showing improving unit economics. Losses narrowed by 26.2% despite a 47% increase in store count — implying significantly reduced per-store losses. New stores were opened in Zhuhai (a new city for Fairwood), signaling expansion beyond existing markets.

The Group plans to open 10–14 new stores in the coming fiscal year, focusing on second-tier Greater Bay Area cities. Management believes the optimised cost structure and business model now address “high potential target markets.” The path to Mainland profitability remains the key catalyst to watch.

4.3 Property Investment

Property rental income of HK$6.5M generated segment profit of HK$10.3M (FY2025: HK$9.6M), reflecting the contribution of investment properties (HK$21.9M book value) plus internal rental allocations.

5. Strategic Transformation Initiatives

Fairwood’s transformation has been built on five pillars:

-

Cost Structure Optimisation — Multi-year programme now complete. Achieved through:

- AI-driven data analytics for demand forecasting, labour deployment, and inventory management

- Aggressive landlord rent negotiations

- Kitchen process re-engineering (streamlined layouts, multi-role staffing)

- Utilities and R&M cost control

-

Quality Enhancement & Executional Excellence — 360-degree process reviews, tightened store audits, enhanced training. Focus on making Fairwood meals “highly enjoyable dining experiences offering strong value for money.”

-

Store Network Optimisation — Data-led approach replacing simple expansion. Consolidating underperformers while opening data-justified new locations. 4–8 new HK stores planned for FY2026/27.

-

Customer Segmentation & Digital Engagement — Moving from generic mass discounts to needs-based segmentation. Fairwood member app, differentiated promotions, KOL marketing on Instagram and Facebook.

-

Mainland China Expansion — Aggressive growth in the GBA. Target: 10–14 new stores in FY2026/27, focusing on second-tier cities. An optimised cost model provides the platform for this push.

ESG & Community: HK$2M meal voucher donation for Tai Po fire victims, 650,000 senior cardholders under “Care for Senior Card” scheme, 232 tonnes of food waste recycled (coffee grounds, lemon rinds at 115 stores), sugar packet reuse programme at all stores.

6. Valuation & Shareholder Returns

| Metric | Value |

|---|---|

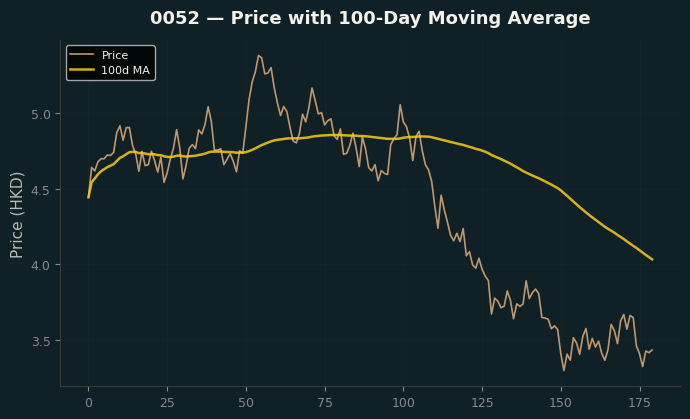

| Last Price (as at data) | HK$4.24 |

| Market Capitalisation | ~HK$549.3M |

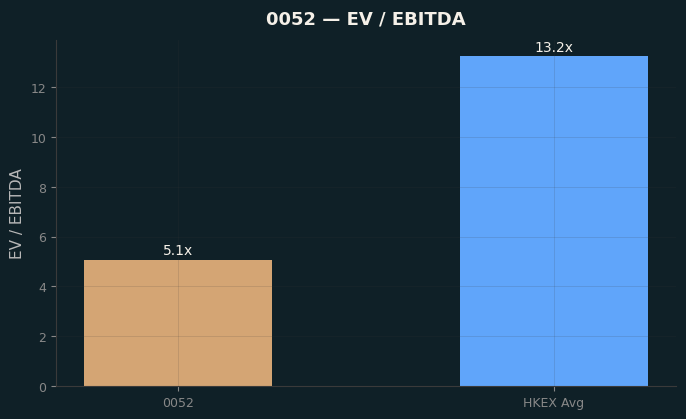

| Trailing P/E | 13.2× (based on HK32.08¢ EPS) |

| Dividend Yield (Trailing) | 7.1% (based on HK30.0¢ DPS) |

| Payout Ratio | ~94% |

| Price / Book | ~0.82× |

| Net Cash Position | ~HK$569.7M (cash less total borrowings) |

| Net Cash / Market Cap | ~103.7% |

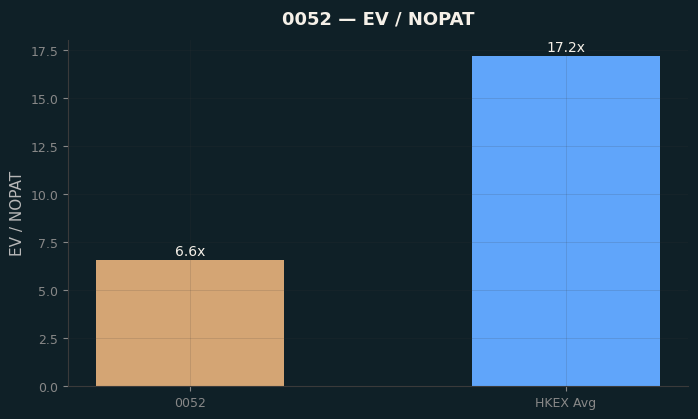

| Enterprise Value | ~Negative (cash exceeds market cap) |

| Return on Average Equity | 6.3% (FY2025: 5.4%) |

Fairwood trades at a striking negative enterprise value — its net cash position of ~HK$570M exceeds its entire market capitalisation of ~HK$549M. The market is effectively valuing the operating business at zero, or even negative after accounting for the cash. This valuation implies extreme skepticism about:

- The sustainability of the HK F&B operating model

- The path to Mainland China profitability

- The structural headwinds facing Hong Kong’s casual dining sector (northbound consumption, changing demographics)

The 7.1% dividend yield is well-covered by operating cash flow but represents a near-full payout of accounting earnings. Any earnings shortfall would require drawing on the cash buffer to maintain the dividend.

Peer context: Comparable HK-listed F&B operators with similar scale (Cafe de Coral, Tam Jai, McDonald’s HK franchisee) typically trade at 12–18× P/E. Fairwood’s discount reflects both its smaller scale and Mainland drag.

7. Risk Factors

| Risk | Assessment |

|---|---|

| Northbound Consumption | Hong Kong residents increasingly dining and shopping in Shenzhen/GBA — structural headwind for HK F&B revenues. Mitigated partially by Fairwood’s own GBA expansion, but HK same-store sales may continue to face pressure. |

| Mainland China Execution | Rapid store expansion (10–14 new stores planned) carries execution risk. The segment is still loss-making; faster-than-expected expansion could widen losses before economies of scale kick in. |

| Food Cost Inflation | Food costs rose to 24.6% of revenue as the Group invested in quality. Further commodity price increases or supply chain disruption could erode the hard-won margin gains. |

| Labour Market Tightness | HK F&B faces chronic labour shortages. Staff costs at 35.3% of revenue remain the largest single expense — wage inflation is an ongoing pressure. |

| Lease Renewal / Rental Risk | Lease liabilities of HK$945M across 184 stores represent significant fixed obligations. Successful rent negotiation in FY2026 may prove hard to repeat if the commercial property market stabilises. |

| Dividend Sustainability | 94% payout ratio leaves minimal buffer for reinvestment or earnings shocks. While cash-rich today, sustained high payouts depend on continued operating cash flow. |

| Competition | HK fast food market is mature with strong competitors (Cafe de Coral, Maxim’s MX, McDonald’s). Price competition could pressure margins. |

| Brand Relevance | The brand revitalisation (new logo, store upgrades) needs to resonate with younger demographics. The risk of Fairwood being perceived as “old-fashioned” relative to newer entrants remains. |

8. Outlook & Investment Thesis

Management’s tone is cautiously optimistic — acknowledging a “challenging and competitive” environment while expressing confidence in the sustainable cost base now in place. The near-term strategy pivots from cost-cutting to top-line growth:

- HK: Modest store expansion (4–8 new stores), continued product quality upgrades, targeted promotions, and growing tourist engagement (Mainland visitors).

- Mainland China: Aggressive GBA expansion (10–14 stores), targeting second-tier cities where growth opportunities are “evident.”

- Digital & brand: Increased advertising spend to support differentiated segment marketing and KOL engagement.

Investment considerations:

Bull case: The market is pricing the operating business at zero. If Fairwood can demonstrate (a) sustained HK margin improvement, (b) Mainland China approaching breakeven, and (c) continued cash generation supporting the ~7% dividend yield, a re-rating towards 10–12× P/E is plausible — implying ~HK$3.85–4.62/share on current earnings, or >HK$6 on any earnings recovery.

Bear case: Structural headwinds (northbound consumption, HK demographic decline, labour cost inflation) persist. Mainland China losses widen with aggressive expansion. The dividend is cut to preserve cash. The market continues to assign zero value to the operating business.

Base case: Fairwood remains a cash-rich, low-growth HK F&B operator generating steady operating cash flow. The 7% dividend yield provides a floor for the share price, while Mainland China remains a multi-year story. The negative enterprise value provides a meaningful margin of safety for income-oriented investors.

Source: Fairwood Holdings Limited Annual Results Announcement for the year ended 31 March 2026, published 30 June 2026.