Executive Summary

Café de Coral Holdings Limited (0341.HK) released its FY2025/26 Interim Report (six months ended 30 September 2025), revealing significant earnings pressure amid a structural transformation of Hong Kong’s F&B market. Revenue declined 5.4% YoY to HK$4,036.2 million, while profit attributable to shareholders plunged 67.6% to just HK$46.7 million. The Group declared an interim dividend of HK10 cents per share (vs. HK15 cents last year), representing a 124.1% payout ratio — a clear signal of management’s commitment to shareholder returns despite near-term headwinds.

The core challenges: (1) normalisation of Hong Kong outbound travel draining weekend/holiday traffic, (2) weak inbound tourist spending, (3) fierce price competition across the F&B sector, and (4) structural shifts in consumer dining behaviour. Management, under CEO Piony Leung and CFO, has launched a comprehensive transformation programme focused on new formats, outlet rationalisation, menu simplification, and supply chain integration.

| Key Metric | H1 FY2025/26 | H1 FY2024/25 | YoY Change |

|---|---|---|---|

| Revenue | HK$4,036.2M | HK$4,264.8M | -5.4% |

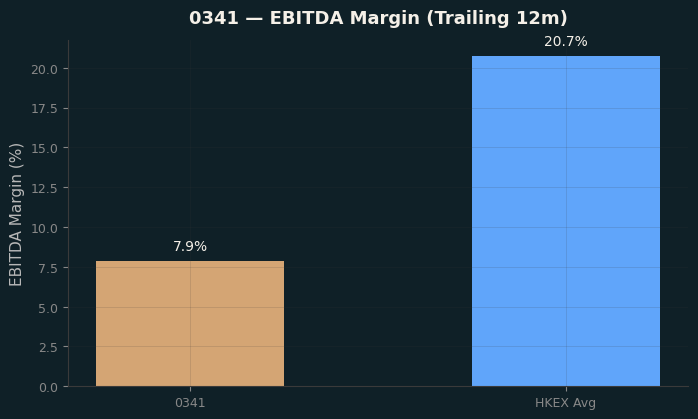

| Gross Profit | HK$329.4M | HK$437.4M | -24.7% |

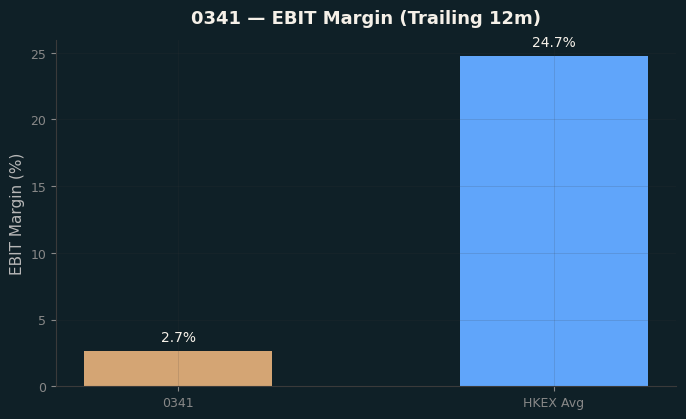

| Gross Margin | 8.2% | 10.3% | -2.1pp |

| Operating Profit | HK$88.4M | HK$189.9M | -53.5% |

| Adj. EBITDA | HK$242.9M | HK$343.8M | -29.4% |

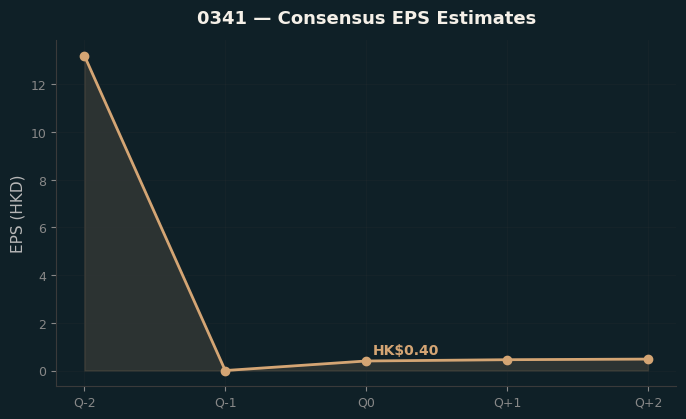

| Profit Attributable | HK$46.7M | HK$144.0M | -67.6% |

| Basic EPS | 8.2 HK cents | 25.0 HK cents | -67.2% |

| Interim DPS | 10 HK cents | 15 HK cents | -33.3% |

1. Financial Performance Analysis

1.1 Revenue by Business Segment

The Group operates a diversified portfolio across Hong Kong and Mainland China:

| Segment | H1 FY2025/26 (HK$M) | H1 FY2024/25 (HK$M) | YoY |

|---|---|---|---|

| HK — Quick Service Restaurants | 2,422.2 | 2,574.0 | -5.9% |

| HK — Casual Dining | 386.2 | 409.0 | -5.6% |

| HK — Institutional Catering | 432.8 | 452.4 | -4.3% |

| HK — Others | 61.0 | 66.3 | -8.1% |

| HK Subtotal | 3,302.2 | 3,501.7 | -5.7% |

| Mainland China | 734.0 | 763.1 | -3.8% |

| Group Total | 4,036.2 | 4,264.8 | -5.4% |

Hong Kong accounts for 81.8% of Group revenue. The Casual Dining and Institutional Catering segments demonstrated relative resilience thanks to simpler operating models and captive demand. Mainland China revenue held up better (-3.8%) with continued network expansion in the Greater Bay Area.

1.2 Cost Structure & Margin Analysis

| Cost Line | H1 FY2025/26 (HK$M) | % of Revenue | H1 FY2024/25 (HK$M) | % of Revenue |

|---|---|---|---|---|

| Raw Materials & Packaging | 1,122.3 | 27.8% | 1,169.4 | 27.4% |

| Staff Costs | 1,395.9 | 34.6% | 1,449.3 | 34.0% |

| Rental Costs* | 482.0 | 11.9% | 499.9 | 11.7% |

| Administrative Expenses | 222.2 | 5.5% | 242.2 | 5.7% |

*Includes ROU asset depreciation, lease finance costs, short-term/variable lease costs.

Gross margin compressed 210bp to 8.2% — the result of price competition and weak consumer sentiment forcing discounting, coupled with Hong Kong’s outbound travel normalisation hitting high-margin peak-period sales. Staff costs as a percentage of revenue rose 60bp to 34.6%, reflecting operating deleverage on fixed labour. Raw material costs also ticked up 40bp to 27.8%.

Management is addressing margins through menu reengineering (focus on core/hero products), operational simplification, and supply chain integration across HK and Mainland China.

1.3 Profit Bridge

Other income and other losses, net swung to a HK$18.8M loss (vs. HK$5.3M loss in H1 FY24/25), driven by:

- Fair value loss on investment properties: HK$11.8M (vs. nil)

- Impairment of PPE and ROU assets: HK$5.6M (vs. HK$6.7M)

- Loss on disposal of PPE: HK$2.0M

Excluding the fair value loss on investment properties, underlying profit attributable declined 59.4% YoY (vs. the headline -67.6%). The adjusted EBITDA of HK$242.9M provides a cleaner picture of operating cash generation capacity.

2. Balance Sheet Analysis

| Item | 30 Sep 2025 (HK$M) | 31 Mar 2025 (HK$M) | Change |

|---|---|---|---|

| Total Assets | 5,790.0 | 5,980.2 | -3.2% |

| Cash & Equivalents | 965.3 | 1,053.6 | -8.4% |

| PPE | 1,411.4 | 1,465.0 | -3.7% |

| ROU Assets | 2,117.8 | 2,159.0 | -1.9% |

| Investment Properties | 390.3 | 402.1 | -2.9% |

| Total Equity | 2,646.6 | 2,744.7 | -3.6% |

| Long-term Borrowings | 125.0 | 225.0 | -44.4% |

| Current Borrowings | 140.0 | 80.0 | +75.0% |

| Lease Liabilities (Non-current) | 1,083.7 | 1,093.3 | -0.9% |

| Lease Liabilities (Current) | 681.3 | 736.0 | -7.4% |

Key observations:

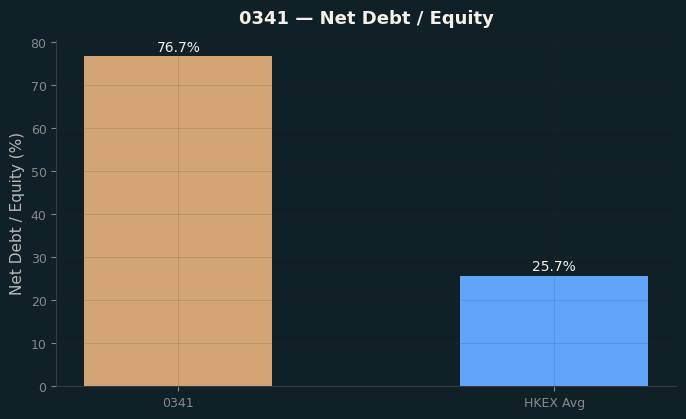

- Strong cash position: HK$965.3M in cash against HK$265.0M in total bank borrowings. Net cash position of ~HK$700M.

- Lease-heavy balance sheet: Total lease liabilities of HK$1,765.0M (both current and non-current) reflect the Group’s extensive retail footprint. This is a structural feature of the F&B industry under HKFRS 16.

- Borrowing profile shift: Long-term borrowings reduced from HK$225M to HK$125M, while current portion increased. Total borrowings flat at HK$265M.

- Net current liability position widened to HK$414.9M (from HK$303.9M), primarily due to the reclassification of borrowings.

- Dividend payment: HK$147.3M in dividends paid during the period (final + interim).

3. Cash Flow Analysis

| Item | H1 FY2025/26 (HK$M) | H1 FY2024/25 (HK$M) |

|---|---|---|

| Operating Cash Flow | 692.3 | 779.5 |

| Investing Cash Flow | (105.7) | (125.4) |

| Financing Cash Flow | (678.8) | (850.0) |

| Net Change in Cash | (92.2) | (195.9) |

Operating cash flow of HK$692.3M remains robust — significantly exceeding reported profit, driven by non-cash depreciation (HK$578.1M including ROU assets). This is the engine that funds dividends and transformation investment.

Investing cash flow improved as capex on PPE moderated to HK$124.1M (vs. HK$156.6M), reflecting more disciplined capital allocation during the transformation period.

Financing outflows of HK$678.8M were dominated by lease liability payments (HK$467.4M) and dividend payments (HK$147.3M). The prior year included HK$46.0M in share buybacks.

4. Business Segment Review

4.1 Quick Service Restaurants (QSR) — HK$2,422.2M, -5.9%

The Group’s largest segment (60.0% of Group revenue) operates 223 stores under the Café de Coral Fast Food (173 stores) and Super Super Congee & Noodles (50 stores) brands.

Same-store sales: Café de Coral Fast Food -7%, Super Super Congee & Noodles -10%. The decline was driven by:

- Weak local consumption and multiple severe weather events (July–September)

- Intensified price competition during breakfast and lunch segments in summer

- Lower traffic on weekends, holidays, and evening dinner segments as outbound travel normalised

Strategic response: Café de Coral Fast Food launched a nostalgic marketing campaign centred on its signature “Hero Baked Pork Chop Rice,” emphasising craftsmanship and quality. The Company has submitted an application to have the dish recognised as part of Hong Kong’s Intangible Cultural Heritage list. The “Club 100” loyalty programme won multiple industry awards (MARKies Awards 2025, DigiZ Awards 2025).

4.2 Casual Dining — HK$386.2M, -5.6%

56 stores across brands: Oliver’s Super Sandwiches (17), The Spaghetti House (6), Shanghai Lao Lao (11), Mixian Sense (18).

Key points:

- Revenue decline primarily from store network rationalisation and optimisation

- Western cuisine brands delivered encouraging profit under simpler operational models

- Shanghai Lao Lao became Hong Kong’s first local brand to offer Shanghainese-style care food (soft meals for elderly), participating in the HKCSS “Care Food” programme

- Focus areas: menu reengineering for margin improvement, guest chef collaborations, membership programmes

4.3 Institutional Catering — HK$432.8M, -4.3%

99 operating units under Asia Pacific Catering and Luncheon Star. This segment demonstrated the most resilience thanks to stable demand from institutional clients (schools, hospitals, corporate canteens).

- Asia Pacific Catering successfully renewed major contracts across all sectors while rationalising underperforming branches

- Luncheon Star saw improving contract renewal rates; actively launching new menus with premium ingredients to drive student market volume

4.4 Mainland China — HK$734.0M, -3.8%

190 stores (up from 185 at FY2024/25 year-end), concentrated in the Greater Bay Area. Despite a challenging economic environment, the Group maintained steady network expansion while exercising strict operational control. Revenue held up relatively well compared to Hong Kong.

5. Strategic Transformation Initiatives

Management has acknowledged the structural nature of market changes and launched a comprehensive transformation under CEO Piony Leung and CFO leadership. Key pillars:

5.1 New Business Formats

- Exploring new operating models specifically for the Fast Food business

- Applying successful Casual Dining playbooks to other segments

5.2 Network Rationalisation

- Consolidating underperforming outlets (HK store count: 378 vs. 381 at year-end)

- Securing high-traffic locations for new stores

- Target: “descaling for future growth”

5.3 Operational Simplification

- Streamlining processes and workflows

- Accelerating digitalisation and automation to reduce labour dependency

- Revamping menu mixes — focus on core/hero products and value offerings

- Maintaining high quality standards that define the Café de Coral brand

5.4 Supply Chain & Cost Control

- Integrating and upgrading supply chains across Hong Kong and Mainland China

- Rent reduction negotiations

- Capex discipline (PPE capex fell from HK$156.6M to HK$124.1M)

- Overhead control and corporate structure simplification

5.5 ESG & Sustainability

- Supplier ESG Assessment Programme launching this year with annual evaluations

- AI-powered energy optimisation: Piloted in Mainland China stores, projecting >20% electricity savings on ventilation and air-conditioning

- Poon Choi Container Recycling Programme: First-of-its-kind initiative rewarding customers for returning cleaned containers

- Silver Economy: Participated in government “Caring Food Coupon Programme,” providing HK$15 breakfasts to 50,000 elderly beneficiaries

- Awards: Best ESG (Environment) at HKIRA 11th Investor Relations Awards 2025; ESG Social Pillar High Achiever Award; “Diamond Enterprise” for 8th consecutive year

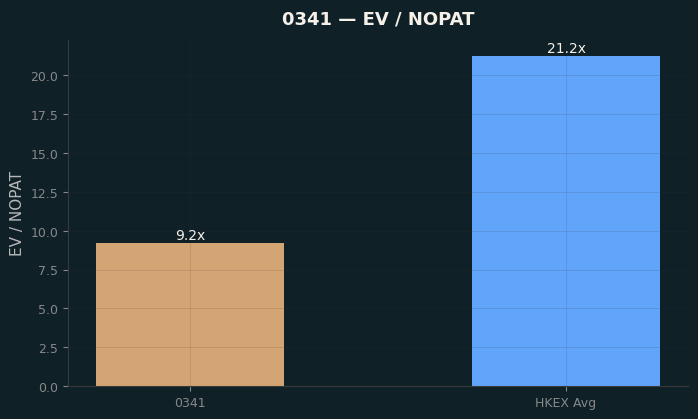

6. Valuation & Shareholder Returns

| Metric | Value |

|---|---|

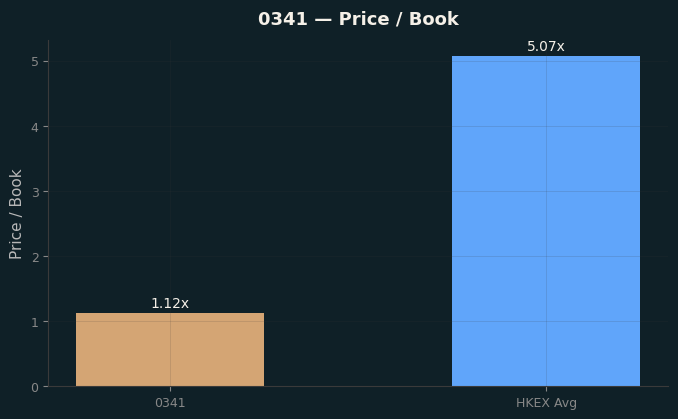

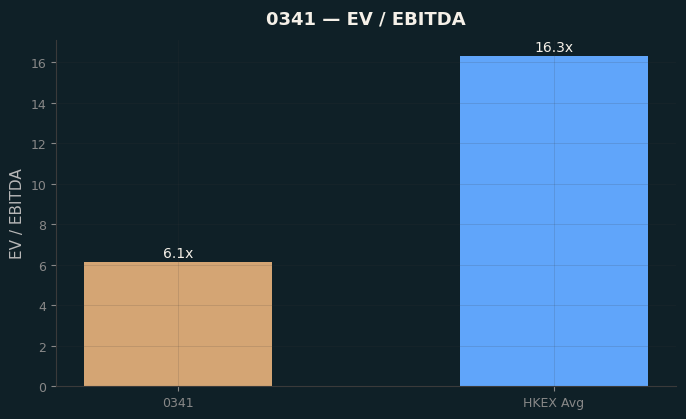

| Trailing P/E | ~10.6x (based on last price ~HK$4.28) |

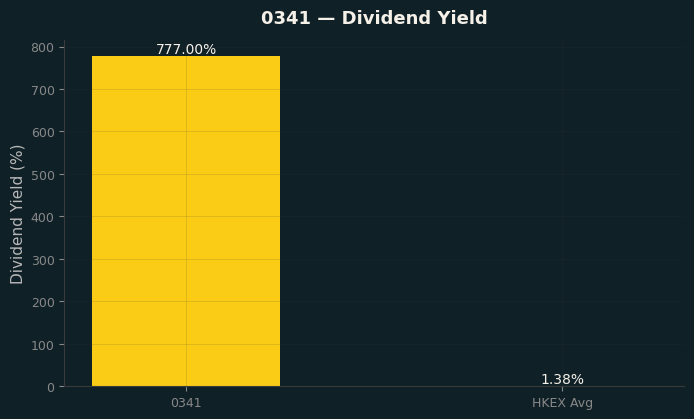

| Interim DPS | HK10 cents |

| Payout Ratio | 124.1% |

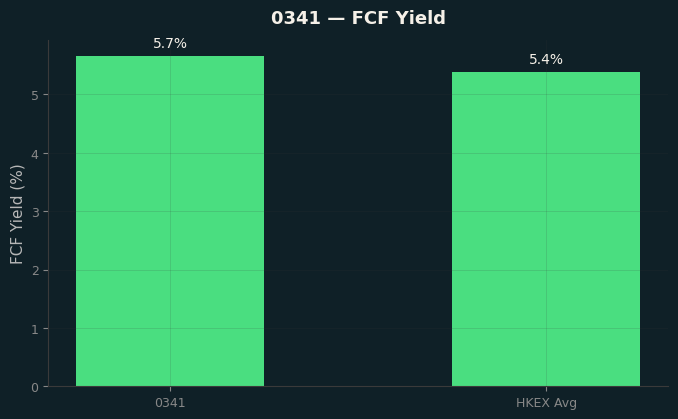

| Dividend Yield | ~4.7% (annualised based on prior final + interim) |

| Net Cash Position | ~HK$700M |

| Market Cap | ~HK$2.48B |

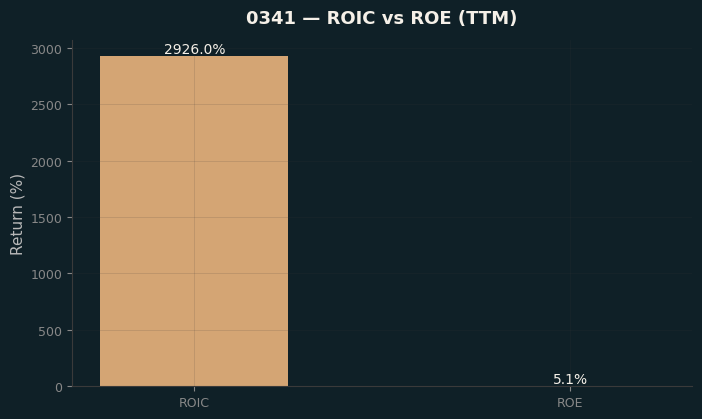

The 124.1% payout ratio for the interim dividend underscores management’s confidence in the Group’s cash generation and balance sheet strength, even as reported earnings compress. The Group has historically maintained generous dividend payouts, supported by the asset-light operational cash flow from its lease-heavy model.

The trailing P/E of ~10.6x appears undemanding, but earnings are at a cyclical trough. A return to even H1 FY2024/25 profitability levels (HK$144M half-year profit) would imply a ~8.6x P/E on an annualised basis.

7. Risk Factors

| Risk | Assessment |

|---|---|

| Structural demand shift | Outbound travel normalisation and changing dining patterns may be permanent, not cyclical — requiring genuine business model adaptation |

| Margin pressure | 8.2% gross margin leaves limited buffer; staff costs at 34.6% of revenue are sticky |

| Competitive intensity | Price war dynamics in Hong Kong F&B, especially breakfast/lunch segments |

| Mainland China macro | Economic slowdown and weak consumer sentiment persist in the Greater Bay Area |

| Lease obligations | HK$1.77B in total lease liabilities — manageable given operating cash flow but a structural fixed cost |

| Transformation execution | Restructuring, menu changes, and supply chain integration carry execution risk |

| Weather & seasonality | Severe weather events (typhoons, rainstorms) disproportionately impact F&B traffic |

8. Outlook

Management struck a cautious but determined tone. The transformation is expected to “take some time,” but the Group is leveraging:

- Brand legacy: 50+ years of Café de Coral brand equity in Hong Kong

- Portfolio diversification: Multi-brand, multi-format strategy across QSR, casual dining, and institutional catering

- Balance sheet strength: Net cash position, strong operating cash flow

- Proven adaptability: Track record of overcoming market challenges over decades

The CEO is leading business revamp and growth investment; the CFO is driving corporate structure simplification and cost efficiency. While H2 FY2025/26 is likely to remain challenging, the transformation initiatives — if executed well — position the Group for margin recovery and sustainable growth as market conditions stabilise.

Bottom line: Café de Coral is a high-quality Hong Kong consumer franchise navigating a structural F&B market reset. The stock offers a ~4.7% dividend yield backed by strong cash flow and a net cash balance sheet. The investment case hinges on whether the transformation programme can restore earnings to pre-downturn levels. At <11x trough earnings with a net cash position, the risk/reward appears skewed favourably for patient investors.