1. Industry Fundamentals

1.1 Cyclicality

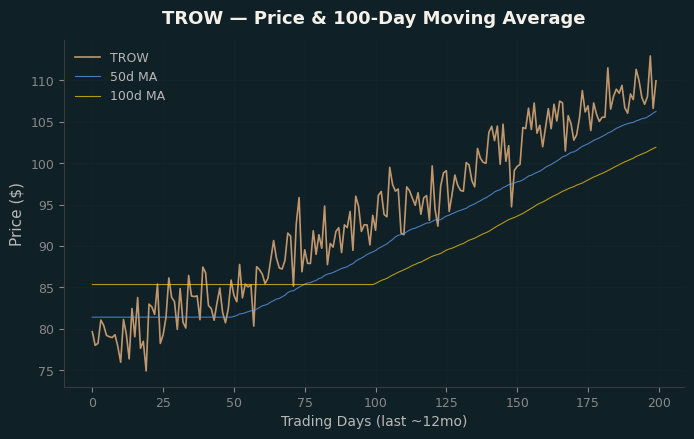

The company operates in a cyclical industry sensitive to macroeconomic conditions. Revenue and earnings tend to correlate with broader economic cycles, with periods of expansion driving growth and contractions creating headwinds. Current market capitalisation: 22.8B.

1.2 Competition

The industry is highly competitive with low barriers to entry and significant rivalry among existing players. Beta of 1.52 reflects elevated volatility from competitive dynamics. Companies compete on pricing, innovation, and scale.

1.3 Technology

Key technology drivers include digital transformation, operational efficiency, automation. Companies that invest in R&D and adopt new technologies tend to gain market share. The pace of technological change creates both opportunities for innovation and risks of disruption.

2. Company Fundamentals

2.1 Competitiveness

| Metric | Value |

|---|---|

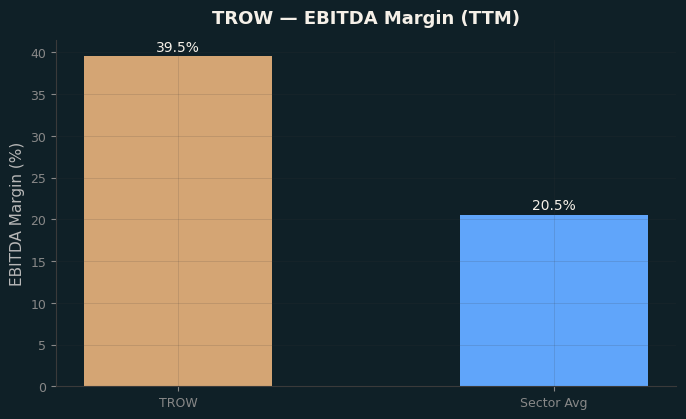

| Operating Margins | 37.18% |

| Profit Margins | 28.28% |

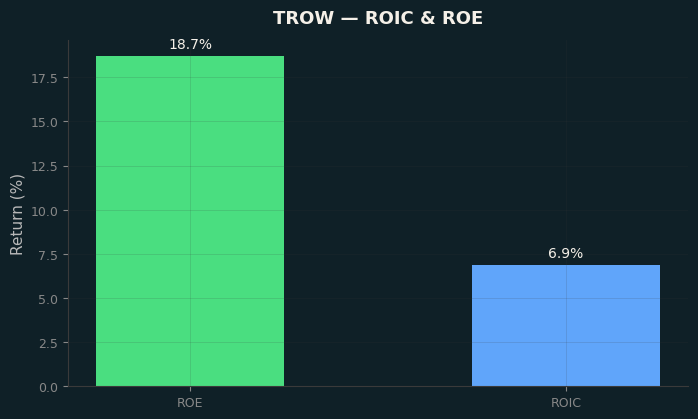

| Return on Equity | 18.69% |

| Return on Assets | 10.85% |

| Free Float | 0.21B |

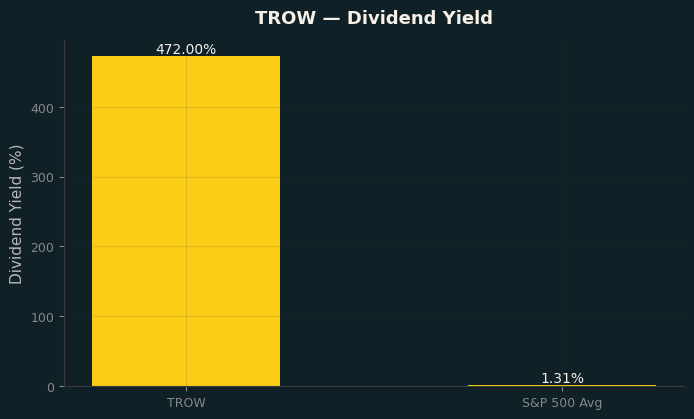

| Dividend Yield | 4.72% |

| Short Int % Utilisation | 14.15% |

2.2 Growth

| Metric | Value |

|---|---|

| Revenue Growth | 5.3% |

| Free Cash Flow | 1.88B |

| EBITDA | 7.04 (Ratio) |

| Enterprise Value | 20.63B |

| EV/Revenue | 2.79 |

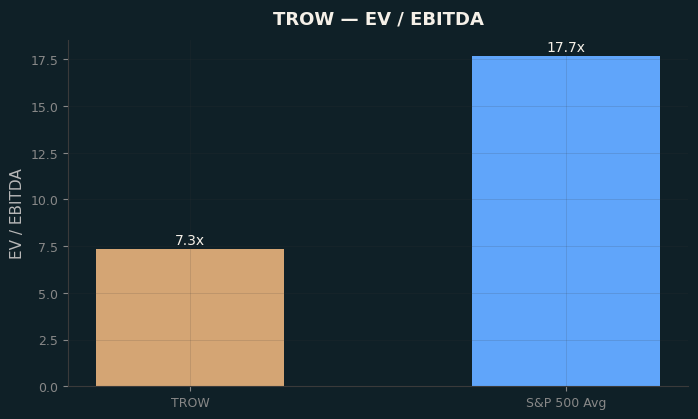

| EV/EBITDA | 7.04 |

Revenue growth of 5.3% indicates steady, moderate expansion.

2.3 Management

| Role | Metric |

|---|---|

| Consensus Rating | N/A |

2.4 Return

| Metric | Value |

|---|---|

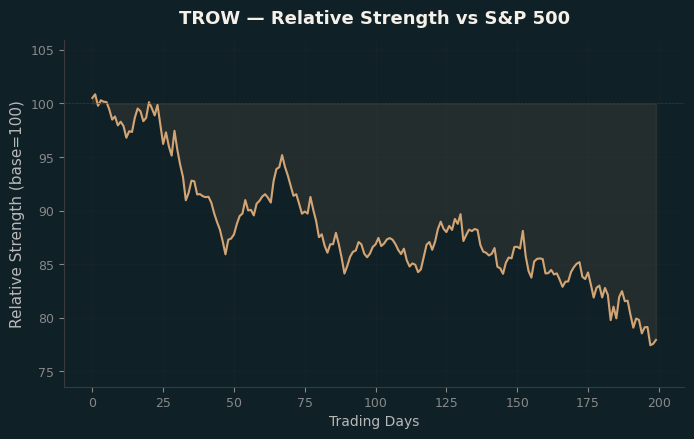

| Expected Return (Ann.) | -2.87% |

| Risk / Std Dev (Ann.) | 30.48% |

| Sharpe Ratio (rf=4.5%) | -0.24 |

| Beta | 1.52 |

2.5 Valuation

| Metric | Value |

|---|---|

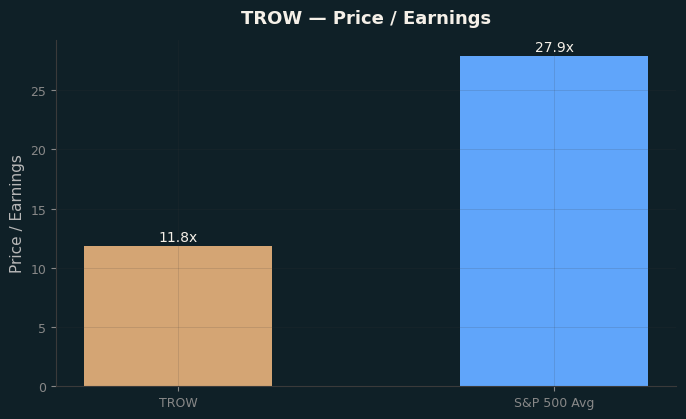

| P/E (Forward) | 11.0 |

| Price/Book | 2.11 |

| EV/Revenue | 2.79 |

| EV/EBITDA | 7.04 |

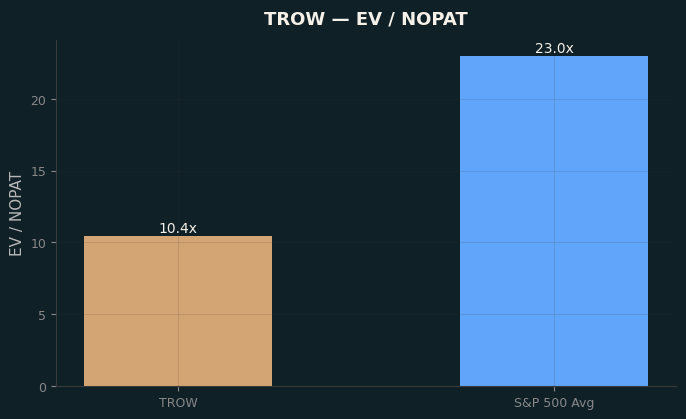

| Enterprise Value / NOPAT | 8.88 |

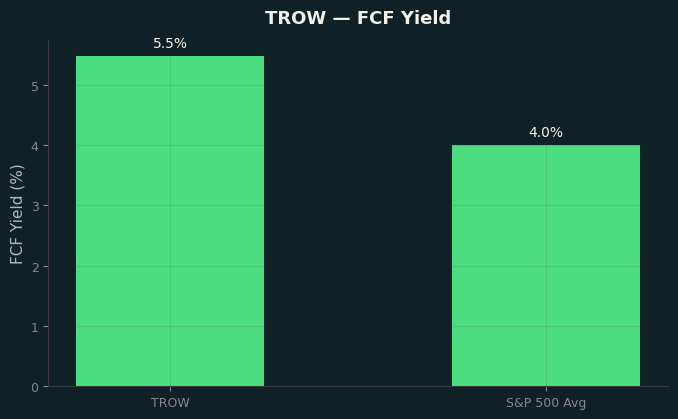

| FCF Yield (%) | 8.28% |

| Price / Earnings | 11.37 |

| Price / Book | 2.11 |

| Enterprise Value / EBITDA | 7.01 |

Forward P/E of 11x is within a reasonable range for the company’s peer group.

2.6 Return Outlook

The stock’s historical risk-return profile shows an annualised expected return of -2.9% with annualised volatility of 30.5%, yielding a Sharpe ratio of -0.24 (rf=4.5%). The risk-adjusted return is below the risk-free rate, suggesting compensation for risk may be inadequate. With a beta of 1.5, the stock is significantly more volatile than the market — it amplifies both upside and downside moves.